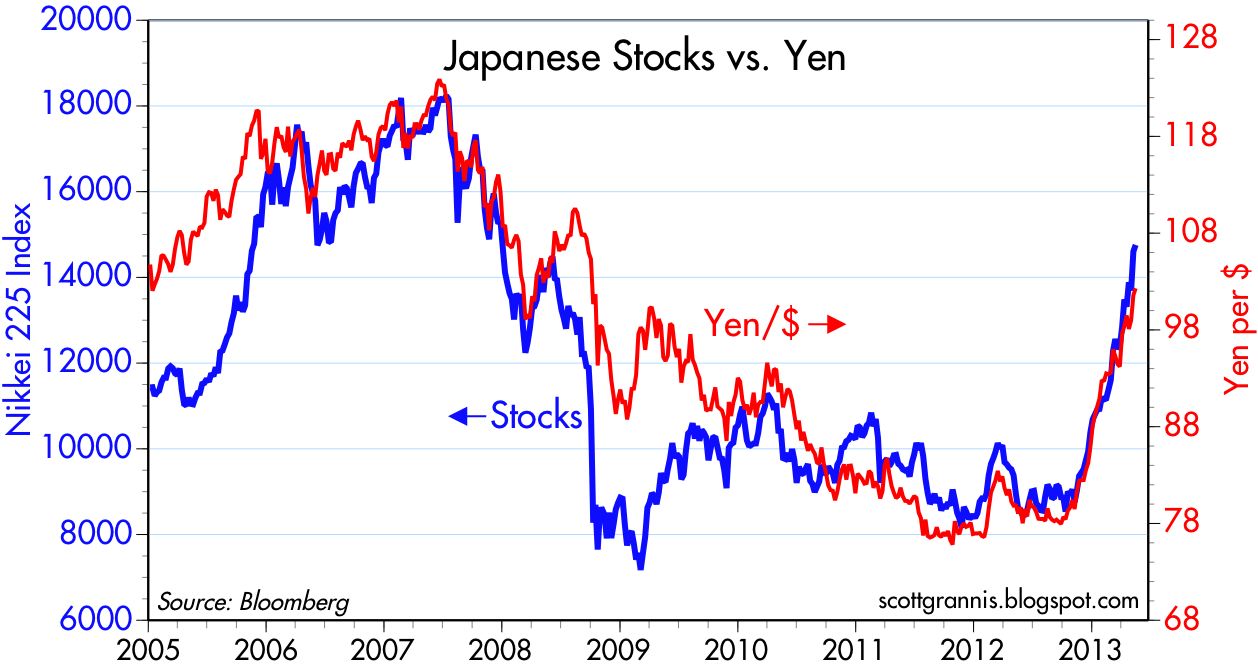

The two charts above compare the National Income and Product Accounts measure of after-tax corporate profits to nominal GDP over different time horizons. Although the growth of corporate profits has slowed in recent years, profits are at or near all-time high levels, both nominally and relative to GDP, with the latter comparison shown in the chart below. In the past 55 years we have never seen such a strong period of profits growth as we have in this recovery.

The fact that corporate profits have tended to track nominal GDP over time is not unusual, but the degree to which profits have outperformed nominal GDP in recent years is exceptional. I've argued for a long time that the market looks at the first chart above and sees a compelling case for corporate profits to revert to their long-term mean (just above 6% of nominal GDP). That would of course imply either a huge decline in profits in the next few years, or an extended period of flat profits, and that helps explain why the market is reluctant to embrace equities. As the second chart above shows, equity flows have been strongly negative for the past six years, even as corporate profits have surged. In short, the market has been behaving as if it were highly skeptical of the durability of corporate profits.

The charts above represent two different ways to judge the valuation of the equity market, both using a ratio of equity prices to earnings. To construct these PE ratios I've used the S&P 500 index as the basis for the "P." In the first chart I've used the NIPA measure of after-tax corporate profits for the "E", and in the second chart I've used the traditional measure of 4-quarter trailing earnings per share for the "E." Both show similar patterns, and between the two of them they suggest that equity valuations are either very attractive (i.e., very low relative to the long-term average), or about fairly valued (i.e., approximately equal to their long-term average). One thing for sure: there is no sign here of any irrational exuberance.

The above chart compares these two measures of corporate profits. Again, very similar, though NIPA profits have grown somewhat faster than S&P 500 earnings per share in the past 30 years and they have been less volatile. I note that NIPA profits tend to lead EPS, and one reason is that NIPA profits are quarterly annualized numbers whereas EPS are 4-quarter trailing profits, so NIPA profits are more contemporaneous. Another reason for the different levels of the two profits measures is that NIPA profits are based on IRS returns, and do not include things such as write-offs that can depress reported EPS. The recent growth of profits by either measure is modest, and it's tempting to think profits might "roll over" in the next year or two. That's what I think the market is already pricing in: a period of very weak growth or the possibility of a recession.

As a counterpoint to the view that profits are so high relative to GDP that they are very likely to revert to the mean, I offer the chart above. This shows that corporate profits are not very high at all when compared to global GDP. Global GDP has grown much faster than U.S. GDP in the past decade, and global sales have become an increasingly important source for the profits of U.S. corporations. So while profits look unsustainably high relative to U.S. GDP, it may simply be the case that, thanks to strong global growth which has greatly expanded the market for U.S.-based corporations, profits are going to move to a new high level relative to U.S. GDP—in other words, the mean is going to shift up permanently. The world has undergone fundamental and significant changes in the past decade, so U.S.-based metrics have become less relevant.

The chart above compares the earnings yield on the S&P 500 (the inverse of the PE ratio) to the real yield on 5-yr TIPS (inverted). The point here is to tie together the messages embedded in stock and bond prices. I think these two series track each other over time because they both reflect the market's confidence in the future health of the economy. When real yields were very high in the late 1990s, equity yields were very low; both were consistent with a market that had a high degree of confidence in the ability of the economy to grow and corporate profits to prosper. Currently, real yields are very low (though they have jumped quite a bit in the past two months) because the market worries that economic growth will be weak, and earnings yields are relatively high because the market worries that corporate profits growth will be disappointing. In short, both tell the same story: the market today is not optimistic at all about what the future holds in store for profits or for economic growth.

The chart above is another method of judging the valuation of equities. It subtracts the 10-yr Treasury yield from the earnings yield of the S&P 500. That gives you the extra yield that investors demand in order to hold equities instead of the safer 10-yr Treasury. The higher the equity risk premium, the riskier stocks are perceived to be. As the chart suggests, the market believes that equities are unusually risky at this time. That fits with my observations above that the market appears to be very worried that earnings are headed for an extended period of weakness.

Now, the market may well prove to be correct, and corporate profits and the economy could tank in the next few years. But to a great extent, that is what the market is priced to. If profits fail to tank and the economy fails to suffer another recession—even if the economy only manages to grow at 2% a year—the market may have to reprice upwards because the future will not turn out to be as bad as is currently expected. Avoiding a recession is all that matters. Long-time readers will know that this is the same story I've been telling for the past four years. The market has consistently underestimated the economy and corporate profits; the rally in equity prices has therefore been a reluctant rally, climbing walls of worry. I don't see a reason to think that anything has changed.